How to Get a Mortgage with No Credit Score

It is commonly understood that you need a decent credit score in order to be approved for large loans, such as a mortgage. However this belief, along with many other beliefs about credit, is a myth. While it is generally much faster to be approved for a mortgage with a good credit score, it is possible to be approved even you have no history of credit, or no credit score. There is a different process used, called manual underwriting, when a person applying for a mortgage has no history of credit. Here is a brief outline of how this process works.

The first step is to talk to your bank or a mortgage agency to determine whether or not they have a manual underwriter on staff. Note that the FHA just recently updated the requirements for manual underwriting so the process may take some time. If you are planning on going through the process, start your conversations with your bank or mortgage agency early.

The underwriter will look closely into your history, bank accounts, current payments (rent, for example) and any other information relating to your finances or finance history. You will most likely have to provide a VOR (variation of rent) that will serve as a resource for determining your reliability of on time payments. The underwrite will also look at your debt to income ratio. This is meant for individuals who have a past of bankruptcy and therefore cannot use their credit score to apply for the loan. Another key element of manual underwriting is reserves. It is expected that you have 1-3 months of reserves (depending on your property) after closing. This is to ensure that you have an emergency fund to pay for the costs of the mortgage after closing.

Before beginning the process, as well as during, it is important not to move large sums of money around. It is also important that you don’t receive large sums of money. This is a red flag as it could indicate a personal loan. Try to keep your finances stable and your financial activity limited to necessary transactions. Also, be sure to have detailed records of any large purchases, expenses, or large sums of money you have received in the past few years. This will help the underwriter sort through your finances much faster and easier.

Talk to your bank, mortgage broker, or local credit union to learn more about the process of manual underwriting and the time it takes to complete the process.

Tags: credit score, mortgage

This entry was posted on at and is filed under Home Mortgage. You can follow any responses to this entry through the RSS 2.0 feed. Both comments and pings are currently closed.

Comments are closed.

-

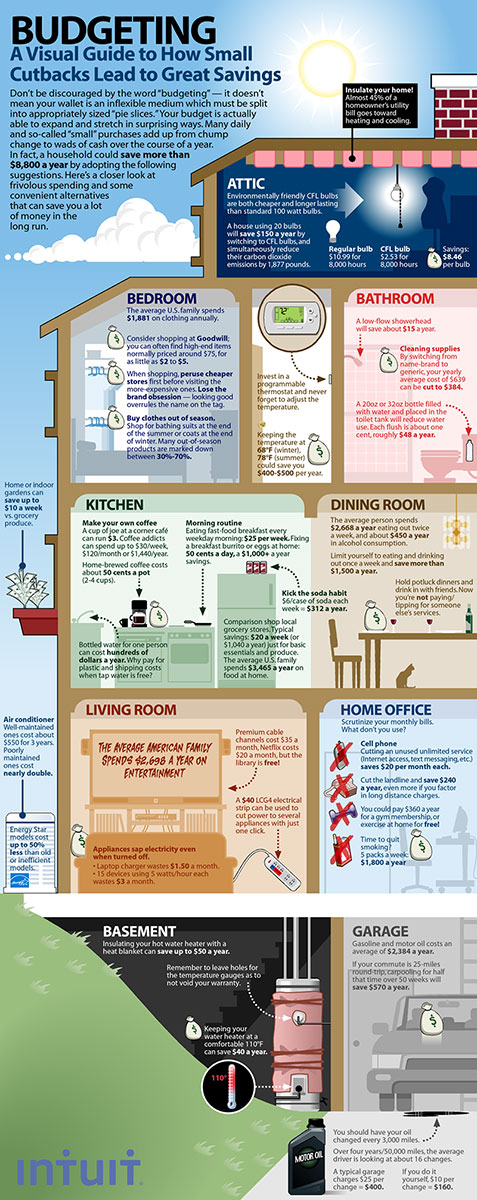

- click to enlarge -