Should You Use Credit Cards or Cash?

It’s no surprise that using credit cards is a major convenience. There’s nothing easier than taking out a small card and using it for your everyday purchases. Unfortunately, the ease of using your credit card is also the cause for millions of dollars worth of credit card debt. Because it’s so easy to simply swipe a card and purchase whatever you want, it’s far too easy to let your spending get out of control. Because of this, one of the most important questions a consumer should ask themselves is whether or not they should be using credit cards or cash? While the answer to this question can vary based upon your income and what you wish to purchase, there are several guidelines all consumers should follow.

Knowing When to Use Credit Cards

Credit cards are an excellent financial tool, when it’s used properly. Unfortunately, many people are unaware of how to clearly determine when using a credit card is acceptable. Because of this, there are a few rules you should go by to ensure you’re always making the wisest financial decisions:

You should always take proper precautions in respect to credit card security. “Follow the standards set forth by your credit card issuer,” says SecurityGuardTrainingCentral.com, “and your chanced of fraudulent activity are substantially diminished.”1

You should never use your credit card when the fee for doing such isn’t the most cost-effective option. While you may think paying your mortgage/rent or any other recurring bill with your credit card is a good idea because you’ll earn reward points, this is just not the truth. Because all credit cards feature interest, if you’re unable to fully pay off the balance, then you’ll actually end up spending more money on these essential monthly purchases. Therefore, always pay cash for such bills.

Should you find yourself facing an unexpected bill, such as a medical bill, you should always negotiate with this creditor before turning to your credit card. In many cases, when you contact the billing department for such bills, you can actually have your balance owed reduced – or an interest-free payment plan – which will ultimately save you money in the long run.

If you’re planning on obtaining a mortgage in the relative near future, you should avoid using your credit cards when at all possible because any changes to your credit report can be disastrous when you’re seeking to open a mortgage loan. Resist the urge to make any major purchases and definitely don’t open a new line of credit. Failure to do so can negatively impact your chances of obtaining a mortgage. Moreover, if you’re in the process of having your mortgage application looked over then you should avoid using your credit cards until the process is complete.

How to Live Debt Free

Living in debt can be stressful and can put unnecessary pressure on families that causes more than just financial problems. About half of the United States population does not have enough money in their accounts to pay of credit card debt each month. That is not even taking into account car loans, student loans, house loans or any personal loans they may have. It is possible to break the cycle of debt and live a debt free life with hard work and determination.

The first step to living a debt free life is to save up an emergency fund. While it is best to save up three to six months worth of expenses, start by saving up $1,000. This is you safety buffer so that the next time an emergency comes along you do not need to put it on your credit card going further into debt.

After you have saved up money in your emergency fund, you can start paying off your debts. Any additional funds you receive above your cost of living should go directly to paying down your debts. Start with the smallest debt you owe first, like a credit card, and then work up from there to your largest debt (probably your house).

Once you have paid off a credit card, try to get rid of it. It is best to live without the temptation and ease of being able to put all of your transactions on there. Instead use cash or a debit card when making purchases. While it is a significant challenge and all members of the household must be on board, living debt free creates peace and freedom. Financial peace and freedom allows you to experience less stress and use your money the way that you want to see it used.

How to Budget – Personal Finance 101

The key to successful financing is a budget. Even the most successful individuals work on a budget in order to keep track of where their money goes. It is important to be in charge of your spending otherwise your money will be in control of you. Budgeting is simply the task of determining what you need to spend money on and assigning each category a dollar amount for the month. They key to successful budgeting is to give every dollar a job. Leftover money creates gaps and opportunities for unnecessary and careless spending.

The first step of budgeting is to sit down with you spouse or partner to plan the budget together. Both parties need to agree on the budget in order to carry it out successfully. If one party feels strongly about one area of the finances, take the time to listen to why this is important and discuss all the impacts it has on the rest of the finances. Once you have assigned jobs for your money the next step is to keep track of every dollar you spend. Even if you use cash for something instead of a credit card, be sure to record the amount. It is likely that there will be surprises along the way and things you did not budget for the first 2-3 months you try this. However, budgeting does get easier and more accurate the longer you stick with it. Over time you will begin to see how valuable it is to live within a budget (and your means). This will also be true if you are saving for a vacation or other large expense. Set aside an amount each month for large expenses so that you can still budget accordingly when the month comes.

Another key component of successful budgeting is planning ahead. Even though Christmas only comes once a year, it is a good idea to budget for it monthly, or at least for a few months before December. This will also be true for quarterly expenses such as insurance, garbage payments, and other bills.

Living on a budget may help you pay all of your bills in full and time (including credit card bills) and may help you to pay down your debts faster. In doing this, you can start to build your credit score. The most common credit score is between 650-700, however you should aim to reach a credit score of 700 or better. The higher your credit score, the easier it will likely be to be approved for loans such as a home mortgage.

How to Get a Mortgage with No Credit Score

It is commonly understood that you need a decent credit score in order to be approved for large loans, such as a mortgage. However this belief, along with many other beliefs about credit, is a myth. While it is generally much faster to be approved for a mortgage with a good credit score, it is possible to be approved even you have no history of credit, or no credit score. There is a different process used, called manual underwriting, when a person applying for a mortgage has no history of credit. Here is a brief outline of how this process works.

The first step is to talk to your bank or a mortgage agency to determine whether or not they have a manual underwriter on staff. Note that the FHA just recently updated the requirements for manual underwriting so the process may take some time. If you are planning on going through the process, start your conversations with your bank or mortgage agency early.

The underwriter will look closely into your history, bank accounts, current payments (rent, for example) and any other information relating to your finances or finance history. You will most likely have to provide a VOR (variation of rent) that will serve as a resource for determining your reliability of on time payments. The underwrite will also look at your debt to income ratio. This is meant for individuals who have a past of bankruptcy and therefore cannot use their credit score to apply for the loan. Another key element of manual underwriting is reserves. It is expected that you have 1-3 months of reserves (depending on your property) after closing. This is to ensure that you have an emergency fund to pay for the costs of the mortgage after closing.

Before beginning the process, as well as during, it is important not to move large sums of money around. It is also important that you don’t receive large sums of money. This is a red flag as it could indicate a personal loan. Try to keep your finances stable and your financial activity limited to necessary transactions. Also, be sure to have detailed records of any large purchases, expenses, or large sums of money you have received in the past few years. This will help the underwriter sort through your finances much faster and easier.

Talk to your bank, mortgage broker, or local credit union to learn more about the process of manual underwriting and the time it takes to complete the process.

Credit Score for Home Mortgage

If you are thinking about purchasing your first home you are probably wondering what type of credit score you need to be approved for a mortgage loan. This depends on the lender you go through and other factors as well, including your income, assets, and how big of a down payment you can afford. The following is some general information related to credit scores and home mortgages.

Large lenders often impose a minimum credit score requirement of around 620. This is fairly low, considering the average credit score in America is 780 as of the most recent data, and anything below credit score of 650 is considered to be a less than optimal for loan qualification. However qualifying for a loan is just part of the process. If your credit score is low, oftentimes your interest rates will be higher. Large lenders often charge higher fees for credit scores below 740, which get increasingly higher with each 20-point drop. Because of this, it is a good idea to work to improve your credit score as much as you can before applying for a home mortgage. You can start to do this by setting a budget and sticking to it, paying off your debts one at a time, and paying all of your bills in full and on time. If your credit score is low because you do not have very much credit history you can work to build your credit history before applying for a home mortgage loan. Start by opening up a credit card and put on only charges you can pay off each month. Pay your bill on time to start building a good history of credit payment. You can also build your credit history with other types of loans as well.

If your credit score falls below the acceptable score for mortgage approval you are not necessarily out of luck. The FHA (Federal Housing Administration) accepts some credit scores as low as 580, however it is a challenge to be approved. The good news is that if you are approved for an FHA loan, there are not additional surcharges based on your score. Be aware that less than four percent of loans approved by the FHA are to individuals with credit scores below 620. It is likely that the applicants that are approved with low credit scores also have a large income and a significant down payment for the home. This is another illustration of why it is very important to improve and maintain your credit score before applying for a home mortgage.

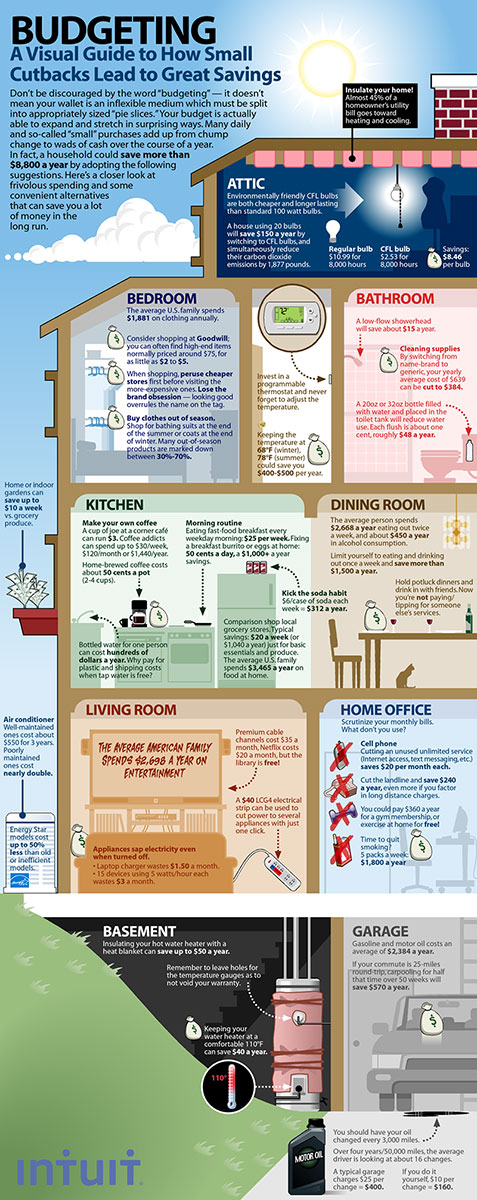

-

- click to enlarge -